Importance of Understanding Compound Interest

Whether you have a savings account or an investment account, you’re benefiting from compound interest. This short read is designed to teach you the basics and benefits of compound interest so you’re one step closer to a financially secure future.

Imagine you have $100 that you would like to put in a savings account. If your savings account offers a 3.65% APR, the following will show you how that $100 will grow over the years.

Initial Investment: $100

APR: 3.65%

1 Year

Interest Income: $3.65 ($3.65 total return)

Account Value: $103.65

2 Years

Interest Income: $3.78 ($7.43 total return)

Account Value: $107.43

3 Years

Interest Income: $3.92 ($11.35 total return)

Account Value: $111.35

As you can see, all you have done is place $100 in a savings account 3 years ago, and you have made $11.35 in interest income.

This may not seem like a lot of money, so let me run you through an example for an investment account. The idea is similar.

Initial Investment: $100

APR: 8%

1 Year:

Total Gains: $8.00

Account Value: $108.00

5 Years:

Total Gains: $46.93

Account Value: $146.93

15 Years:

Total Gains: $217.22

Account Value: $317.22

30 Years:

Total Gains: $906.27

Account Value: $1,006.27

You can see here that in an investment account that averages 8% APR over a 30-year term (which is on the conservative side when long-term investing in an S&P 500 Index Fund), you made a free $906.27 for simply letting your money sit in the market.

Now for the full example and an explanation of all the components together.

Age: 18

This is the earliest you are allowed to open an investment account on your own in the United States.

Account: Roth IRA

A Roth IRA is a tax-advantaged retirement investment account; more on this later.

Initial Investment: $0.00

You are starting your account without investing any money.

Monthly Contribution: $625

You deposit and invest $625 per month, which equals the $7,500 annual limit rule of a Roth IRA

If you are above the age of 50, you can invest an extra $1,000 annually as a “catch-up”.

APR: 8%

APR stands for “annual percentage yield.” This is essentially the percentage earnings you will make each year on the value of your account. This is a low-ball estimate for this example.

Time Frame: 41.5 years

41.5 years after the age of 18 is age 59.5, which is the earliest you can start making penalty-free withdrawals from your Roth IRA account. You may be subject to penalties on capital gains if you need to withdraw early.

Security: Any S&P 500 Index Fund (ex., VOO or SPY)

An S&P 500 Index Fund is basically a basket of 500 of the largest U.S. companies aimed to mirror the performance of the S&P 500 stock market index. This provides investors with diversification across a wide range of U.S. companies and industries. Instead of bearing the risk of buying 1 or 2 stocks, you get the peace of mind that if 1 of the 500 stocks plummets in value, you have 499 other stocks in your portfolio that will smooth out the overall performance.

Assume you open up your Roth IRA investment account on your 18th birthday, which is the earliest age in the U.S. where you are legally allowed to trade on your own.

Each month, you contribute $625 into the same investment account. (max annual contribution for those under 50 years old is $7,500, as of 2026). So, $7,500 divided by 12 months = $625 per month.

You do this for 41.5 years until the age of 59.5 (the earliest legal retirement age)

The security you buy averages an 8% return over these years.

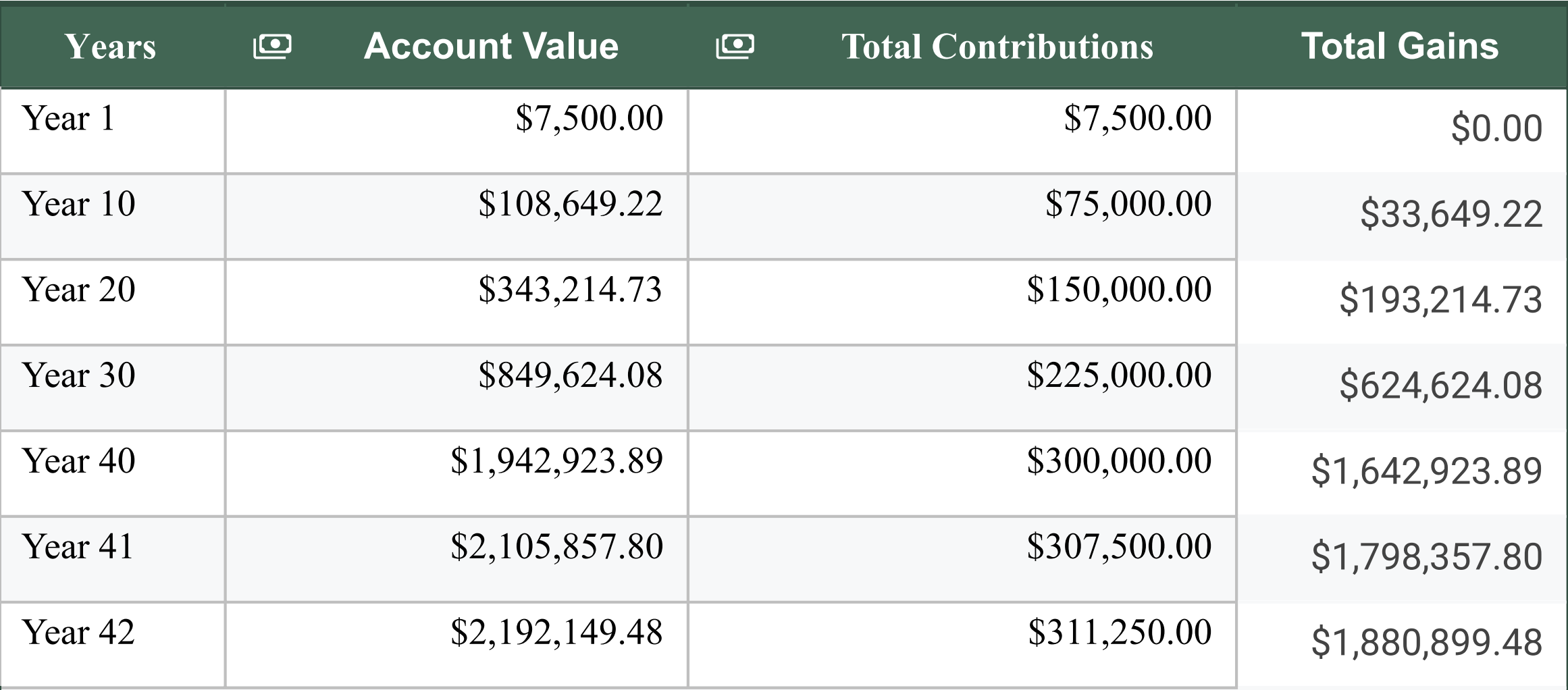

With these assumptions in place, which are again conservative in terms of APR, the following illustrates your account value over the years.

*Chart depicting estimated account value growth over a 41.5-year time frame at 8% APR. This estimate is based on a prediction that a Roth IRA account invested in an S&P 500 Index Fund will produce these results. These results are only a simulation. When investing in the stock market, you must first understand the risk that you may lose money, and no investment is ever a guarantee.

Explanation of Results: After 41.5 years of investing (Year 42) $7,500 every year (or $625 per month), your estimated account value at retirement is $2,192,149.48. You only invested $311,250 over this time period and have made $1,880,899.48 in long-term capital gains. You may be wondering now, what is a Roth IRA? A Roth IRA is a tax-advantaged retirement investment account that allows you to withdraw earnings tax-free at retirement age. This means that you are allowed to start withdrawing money from this account and pay 0 tax on it. Pretty awesome, huh?

Now I understand that shelling out $625 per month is not easy for the average person today. This example illustrates what happens if you max out your Roth IRA contributions each year.

How do I do this?

If you have any questions, email me at bradenvitellifinance@gmail.com. I will add an anonymous Q&A section beneath here with answers and resources for you.